The appraisal industry is under pressure from every direction — a shrinking workforce, mounting regulatory complexity, and growing demand for faster, more consistent valuations. A new class of AI-powered APIs is poised to change that equation.

A Profession at a Crossroads

The numbers tell a sobering story. According to industry data, the appraiser shortage affected 68% of U.S. mortgage transactions in 2023, and average appraisal turnaround times of 12 days delayed 22% of all closings that year. Meanwhile, the active appraiser workforce — some 78,000 credentialed professionals — is contracting at roughly 2.6% annually, driven largely by an aging cohort facing retirement. The U.S. Bureau of Labor Statistics projects about 6,300 new openings per year through 2034, far below what’s needed to reverse the decline.

The problem isn’t just supply. It’s also the sheer weight of manual labor embedded in every appraisal. A typical residential report requires an appraiser to manually collect and validate property details, take and organize on-site notes, classify photos, select and score comparable properties, and populate complex GSE-compliant forms — all before a single analytical judgment is made. The traditional workflow is filled with time sinks and opportunities for human error that no amount of industry goodwill can fully overcome.

Layered on top of this is the coming wave of regulatory change. The UAD 3.6 update, moving toward full implementation in 2026, represents the most significant overhaul to appraisal reporting in over a decade. The new modular, dynamic structure demands greater data granularity, tighter compliance, and more precise property characterization than the old static URAR ever required. Appraisers relying on manual data entry and legacy software face significant productivity declines during the transition — while those leveraging advanced, AI-powered platforms stand to gain a meaningful competitive edge.

The window for that advantage is opening right now.

What Computers Can Now See in a Photograph

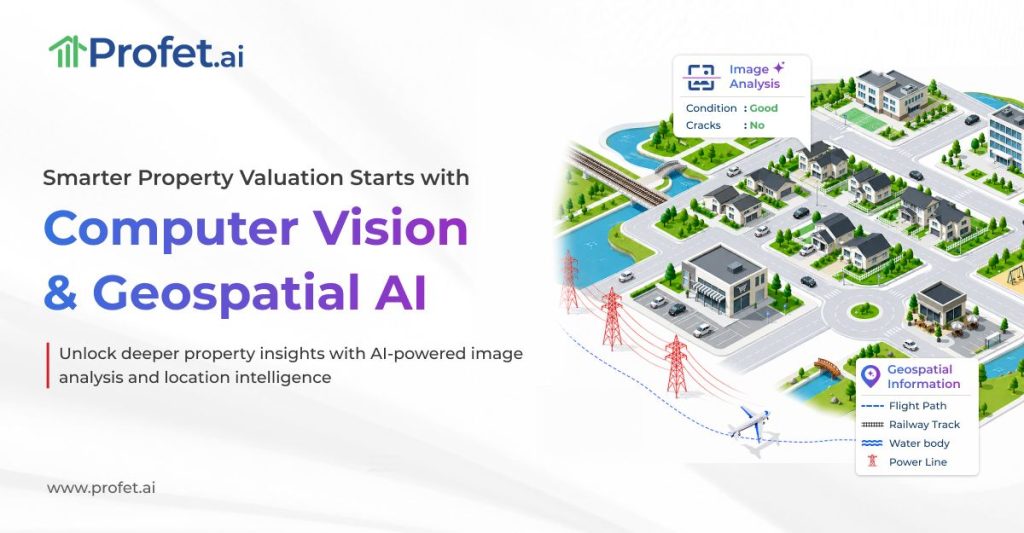

Property photos have always been central to appraisals, but they’ve historically been treated as documentation rather than data. That’s now changed.

Computer vision — the application of machine learning to image analysis — can extract structured, quantitative information from property photographs in seconds. Where an appraiser once had to manually note the presence of hardwood floors, granite countertops, stainless appliances, or a finished basement, AI can now identify, classify, and report those features automatically and consistently across thousands of images.

PropMix, a data and analytics company serving the real estate and mortgage industries, has built a suite of Computer Vision APIs specifically engineered for property valuation use cases. The capabilities span the full range of features that appraisers are required to assess:

Structural and Interior Features — The APIs extract information about structure and design, interior finishes, fixtures, appliances, utilities, basement and attic details, and parking configurations. These are precisely the fields that populate the labor-intensive “Improvements” section of appraisal reports.

Amenities and Exterior Features — From swimming pools and play areas to exterior condition and surrounding landscaping, the system identifies the amenity details that influence both marketability and value.

Property Condition and Quality Ratings — One of the most consequential capabilities is the ability to derive FHFA-standard Condition (C1–C6) and Quality ratings directly from photos. These ratings, required by Fannie Mae and Freddie Mac, have traditionally been among the most subjective elements of an appraisal — a persistent source of inconsistency and, in some cases, bias. AI-driven scoring applies a standardized methodology across every property it touches, including nuanced cases where, for example, a home has a renovated kitchen but dated bathrooms. Automated valuation models using AI-derived condition and quality scores have shown up to an 18% decrease in mean absolute error rates — a meaningful improvement in predictive accuracy.

Damage Detection — The APIs can flag potential property damage visible in photographs, helping corroborate condition ratings and support repair cost estimates. This is particularly valuable in distressed property, REO, and renovation loan contexts where condition assessment carries outsized financial significance.

GSE Compliance Checking — A less obvious but critically important function is automated photo compliance checking. GSE guidelines prohibit appraisal photos from showing people, license plates, pets, and certain signage. Manually reviewing every photograph for these violations is tedious and error-prone. Computer vision can screen the entire photo set instantly, flagging non-compliant images before submission — reducing the risk of costly appraisal revisions and lender pushback.

What Location Intelligence Adds to the Picture

Even the most thorough photo analysis has limits. A photograph can reveal what’s inside a home and what’s immediately outside, but it cannot tell you what lies beyond the frame — and in real estate, context is everything.

PropMix’s Geospatial APIs are designed to fill that gap, enriching photo-derived property data with the location-based factors that appraisers have always had to assess through time-consuming field observation and research. The platform identifies a property’s nearby environmental influencers — power lines, railroad tracks, busy highways, superfund sites, waterbodies, industrial facilities, and cemeteries — any of which can significantly affect market value and must be disclosed in standard appraisal reports.

Beyond negative influences, the Geospatial APIs also capture value-positive location factors. Is the property on a waterfront? Is it a corner lot or positioned in a cul-de-sac? What is its cardinal orientation — east, west, north, or south facing? These details affect everything from natural light and privacy to lot premiums and buyer preference, and they’ve traditionally required manual GIS lookups or physical site observation to document.

When computer vision and geospatial analysis operate together, they create a holistic property intelligence layer that captures both what a home is and where it sits — the two foundational inputs to any defensible valuation.

The Productivity Math

The broader picture: AI-powered valuation tools can reduce valuation error by 2–3% in large-scale studies, with image-derived features accounting for a significant share of top predictive signals. When compounded across a portfolio of thousands of loans, even modest error reductions translate to meaningful risk reduction for lenders.

Feeding Higher-Order Intelligence

Perhaps the most important thing to understand about these APIs is what they’re not — they are not autonomous appraisers. They are data engines.

The hybrid model — AI pre-screens and auto-populates, appraiser confirms and analyzes — is quickly emerging as the industry consensus best practice. It preserves professional oversight while capturing the full productivity dividend of automation.

The Regulatory Tailwind

The timing is not incidental. The appraisal industry is under simultaneous pressure from GSEs, regulators, and lenders to improve consistency, reduce bias, and demonstrate defensible methodology. All three of those demands are served by AI-assisted approaches.

Automated condition and quality scoring reduces the subjectivity that has drawn fair lending scrutiny. Automated compliance checking reduces the risk of GSE repurchase demands. And the structured, auditable data outputs of computer vision APIs provide a documentation trail that manual workflows often lack.

As the UAD 3.6 transition accelerates through 2025 and 2026, the data requirements embedded in the new reporting framework will increasingly favor practitioners and platforms that can source, structure, and validate property data at machine speed. The manual approach will become not just slower, but structurally disadvantaged.

What This Means for Valuation Professionals

And perhaps most importantly: the appraiser who embraces these tools isn’t being replaced. They’re being amplified — freed from the mechanical burden of data collection to spend more time doing the work that only a trained human professional can do.

Please see our press release on this here